UK mortgage lenders

UK mortgage lenders

Current data on UK mortgage lenders #ukmortgages #ukhousing

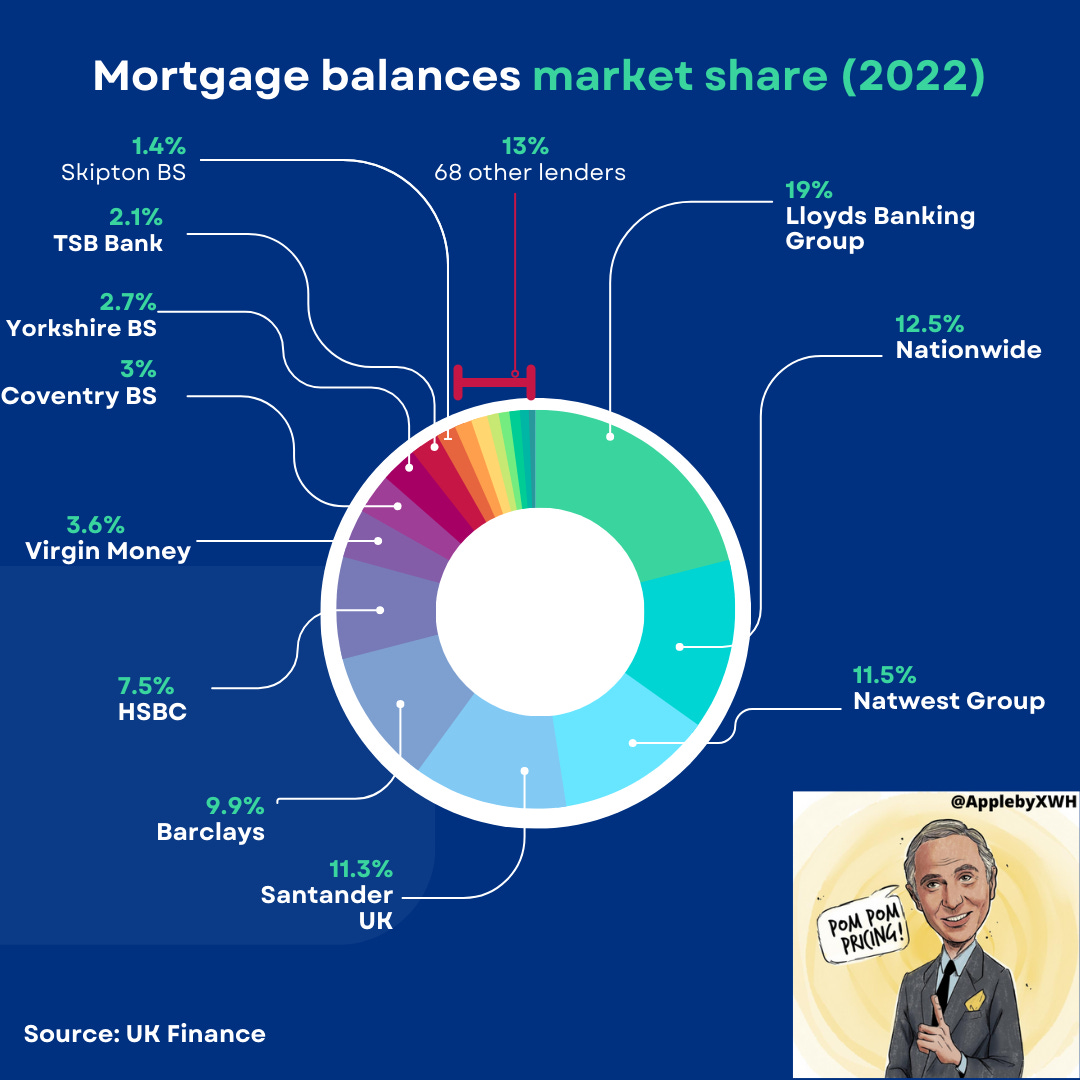

Currently there are approximately 79 mortgage lenders operating in the UK market with outstanding mortgage balances of £1,587bn as of end of 2022. The largest 6 players cover 72% of the mortgage market including Lloyds, Nationwide, Natwest, Santander, Barclays and HSBC based on data from UK Finance1.

Lloyds Banking Group has the largest market share with 19% of mortgage balances, followed by Nationwide (12.5%), Natwest (11.5%), Santander (11.3%), Barclays (9.9%) and HSBC (7.5%). This data suggests that any policies or risk appetite by these six banks would have ripple affects on the rest of the mortgage market and effectively set how much prospective buyers can borrow to buy a home.

In contrast, the smallest 68 mortgage lenders represent only 13% of the 2022 mortgage balances with a total mortgage balance of £213bn, less than Lloyds’ mortgage balance.

By reviewing the market share of the UK based mortgage lenders, there are questions that spring to mind to assess to what extent these mortgage lenders are resilient to a potential mortgage crunch. These questions can include (i) what portion of the outstanding mortgage balances of £1,587bn are covered by customer bank deposits? (ii) is this portion large enough to avoid a mortgage credit crunch? and (iii) how much would these mortgage balances increase due to a rise in interest rates?

https://www.ukfinance.org.uk/system/files/2023-07/MM10.xlsx