Historic total returns of London residential properties

Historic total returns of London residential properties

Comparing historical total returns of London properties against mortgage rates #pompompricing #ukmortgages #ukhousingmarket

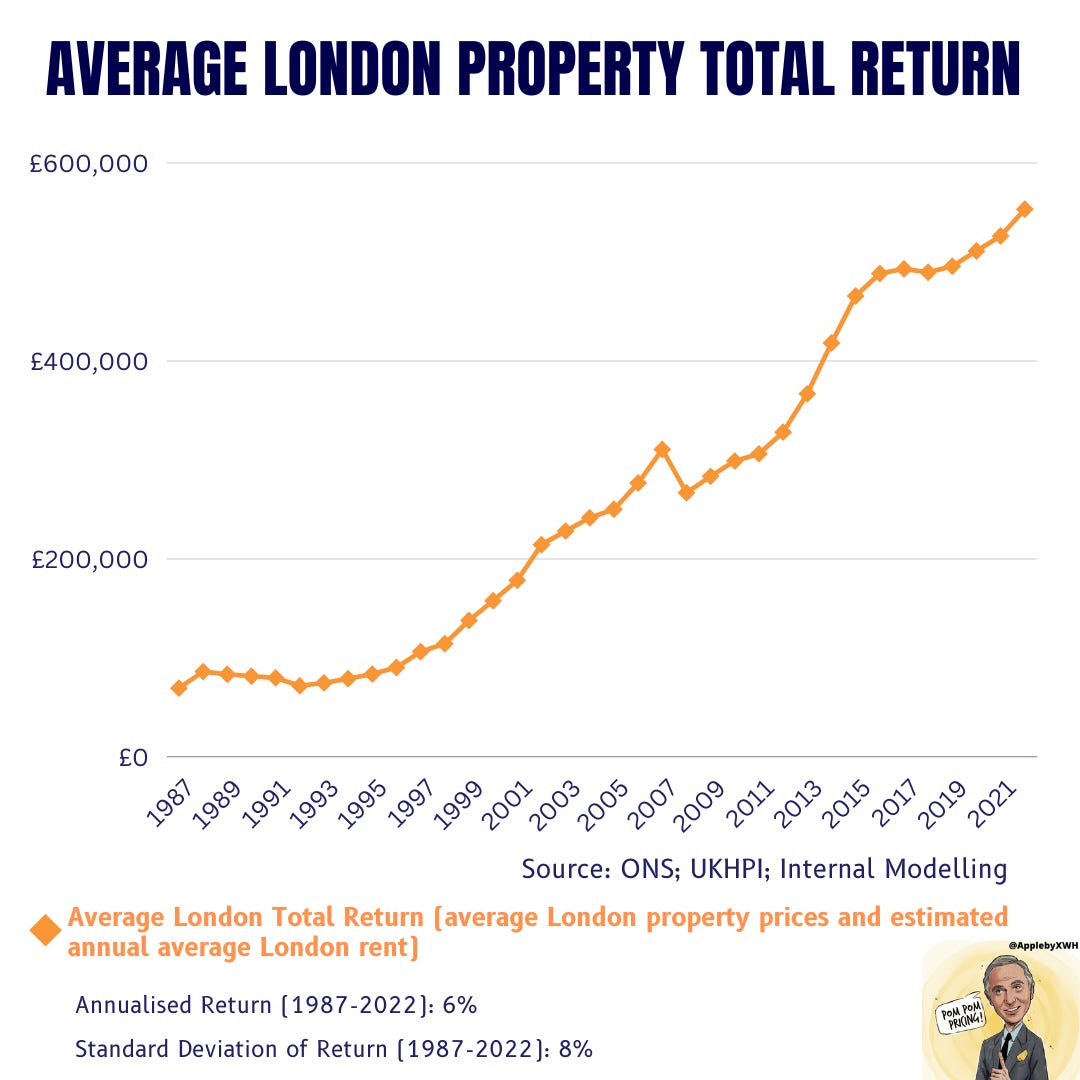

Based on internal modelling along with data from ONS and UK HPI, on average London residential properties have generated annualised total returns of 6% per year since 1987 to 2022. These total returns consist of capital appreciation (i.e. how much London property prices have increased by on average) as well as average London rent (i.e. how much rent received on the average property).

The estimated London property total returns were based on a few key inputs and calculations. The data on average London property prices was derived from the UK House Price Index1 (“UKHPI”).

Whilst, the average London rent required modelling and a few assumptions. Initially, the inputs for this figure included median annual London rents from the Valuation Office covering 2011 to 20192. Whilst, estimating annual rents from 1987 till 2022 relied on inputting the median annual London rents (likely from 2011 and 2020) and re-basing them to give a figure of average London private rents on an annual basis from 1987 till 2022. This re-basing was calculated based on the private rental price index (on a national level) via the Office for National Statistics (“ONS”)3. This re-basing calculation assumed that the rental price index (namely how much private rents increase by on a yearly basis from 1987 onwards) on a national level is the same level applied to London private rents. Whilst this estimate may be incomplete this is the best way the average London private rents with significant data from 1987 given limited data.

igure 2 shows that total value of London property prices and estimated annual London rent has increased year on year (except for drops in the early 1990s and in the Great Recession in 2007). Whilst this might appear as positive news for home buyers it is worth considering whether there is a market correction due or whether the pattern of 6% annualised return can continue. Also, it is worth considering is 6% annualised return worth it if mortgage rates are high at approximately 7%4 ? Would it be worth paying 7% in annual mortgage interest if historic annualised return is only 6%? Is it really worth paying the 1% extra per year on the value of your property ?

https://landregistry.data.gov.uk/app/ukhpi/browse?from=1986-06-01&location=http%3A%2F%2Flandregistry.data.gov.uk%2Fid%2Fregion%2Flondon&to=2021-02-01&lang=en

https://data.london.gov.uk/dataset/average-private-rents-borough

https://www.ons.gov.uk/economy/inflationandpriceindices/timeseries/dobp/mm23

https://news.sky.com/story/cost-of-living-latest-predictions-for-this-weeks-interest-rates-decision-average-mortgage-rates-almost-7-cost-of-booze-going-up-tomorrow-12615118